Personal Finance Is More Personal Than Finance

What I’ve Learned About Money (So Far)

I’m Ekam — currently between things, mildly bored, and overly caffeinated — so I figured why not start sharing stuff I actually enjoy?

Before we dive into my eight post, here’s my story in five words:

Startups. Consumer/Food. Personal Finance. Chess. Sports.

That’s the vibe. If you’re into any of those, stick around.

In July 2023, I had just graduated and was about to start my first job at a startup. I still remember receiving my first proper paycheck , it was a surreal moment. But instead of excitement, I was hit with a strange anxiety:

What am I supposed to do with this ? Should I save it? Spend it? Invest it? How much risk is too much?

That moment marked the start of a deep dive into the world of personal finance. I went down the rabbit hole of watching thousands of videos, listening to podcasts while cooking and going deep.

One voice stood out to me: Morgan Housel

His take on behavioral economics, financial psychology, and storytelling is unlike anyone else. He made finance feel less like numbers and more like life. And that’s what this Substack is about :- not investment advice, but ideas. Stories. Observations. Lessons that stuck with me.

Here are some of my favorite reflections:

1. Risk Is What You Don’t See Coming (A.K.A. Predictions Are Hard)

History is a record of surprises. Prediction is trying to use that record to forecast more surprises. See the problem?

Think about it: the 2008 financial crisis, the COVID-19 pandemic, the Dot-com bubble. All of them were outliers, yet they’ve become anchor points for how we now try to predict the future. Before COVID hit, newspaper headlines barely hinted at what was coming. We’re terrible at seeing the next big thing — because by definition, risk is what you don’t see coming.

In investing too, uncertainty rules. The Big Tech AI arms race — from Tesla’s humanoid robots to Google’s Gemini and OpenAI’s GPT models — who wins?

The honest answer: I don't know.

We all know someone who’s said: “If I had just held one Bitcoin…” “If I had kept my Nvidia stock…”

But hindsight isn’t a strategy.

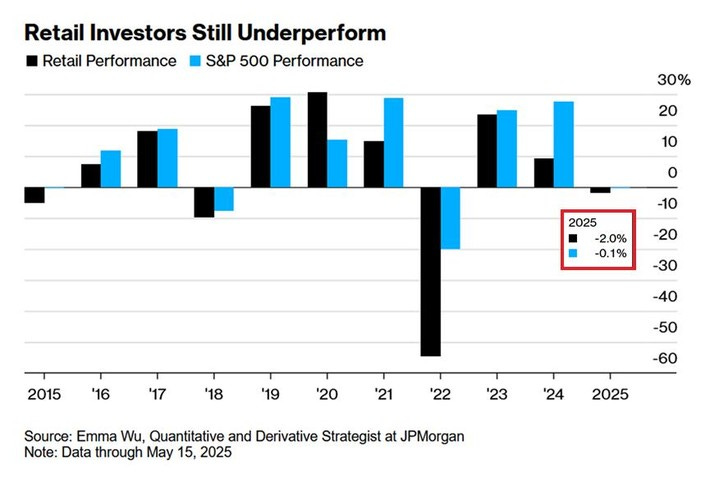

Here are the actual numbers to prove it ; Retail investors still underperform and have been for the past 5 years. The data consistently shows that trying to time the market, chasing hot stocks, and reacting emotionally leads to worse results.

The truth is: No one has a crystal ball. The goal isn’t to guess right. It’s to build a system that works even when you’re wrong.

2. Compounding = Principal × Time × Return. But everyone only talks about return.

Ever noticed how every YouTube ad, financial influencer, or mutual fund agent is obsessed with returns? But compounding isn’t just about returns. It’s a function of three things:

Principal × Time × Return

What if we focused just as much on increasing our principal (income, savings rate) and time horizon (patience, long-term mindset), instead of chasing an extra 2% return?

Your 20s and 30s are a golden opportunity to do this. The earlier you start, the less spectacular your returns need to be. A 12% return from index funds may sound boring compared to the hype of cryptocurrency but 12% compounded over 30 years is wealth.

3. Pessimism Sounds Smart. Optimism Builds Wealth.

Tell someone the market will crash and you sound intelligent and worldly. Say the market will keep growing over the long run and you sound naive.

But history shows that progress, not collapse, is the default long-term trend.

I was chatting with some of my dad's friends the other day, and they brought this idea to life. They explained that if someone had a heart attack in the 90s, their chance of survival was slim. Now? You have a very good chance of not only making it but living a long, healthy life afterward.

The world is so much better in thousands of ways like this. We have everything around us. From driverless cars and mind-bending technology to constant medical advancements, progress is undeniable. The fact that many of our biggest daily problems aren't life-or-death situations is a testament to how far we've come.

If there is one thing I am sure of, it’s that we are going to be fine.

This isn’t just a feel-good story; it’s a powerful investment thesis. The world isn’t perfect, but it gets better, more innovative, and more resilient over time. And your money should reflect that fundamental belief in progress.

This isn’t an investment post. It’s a mindset post.

And if you’re curious for a deeper dive, here’s my first Substack post on building a beginner's personal finance framework.

I completely agree with the fact that before COVID hit, "headlines gave us no real clue of what was about to unfold". Market did in a way though. And that's true for every "crisis". Market is all aboit perception and that’s exactly the point I try to make with my new substack: it’s not the content of the news that signals risk, it’s the structure. The volatility. How narratives form, spread, and shift that’s where the early signals often hide. Anyway interesting view so subscribed!